Solvency (1) - Quick Ratio

|  |

Solvency (2) - Current Ratio

|  |

Solvency (3) - Current Liabilities to Net Worth Ratio

|  |

Solvency (4) - Total Liabilities to Net Worth Ratio

|  |

Solvency (5) - Fixed Assets to Net Worth Ratio

|  |

Efficiency (1) - Collection Period Ratio

|  |

Efficiency (2) - Net Sales to Inventory Ratio

|  |

Efficiency (3) - Assets to Net Sales Ratio

|  |

Efficiency (4) - Assets to Net Working Capital

|  |

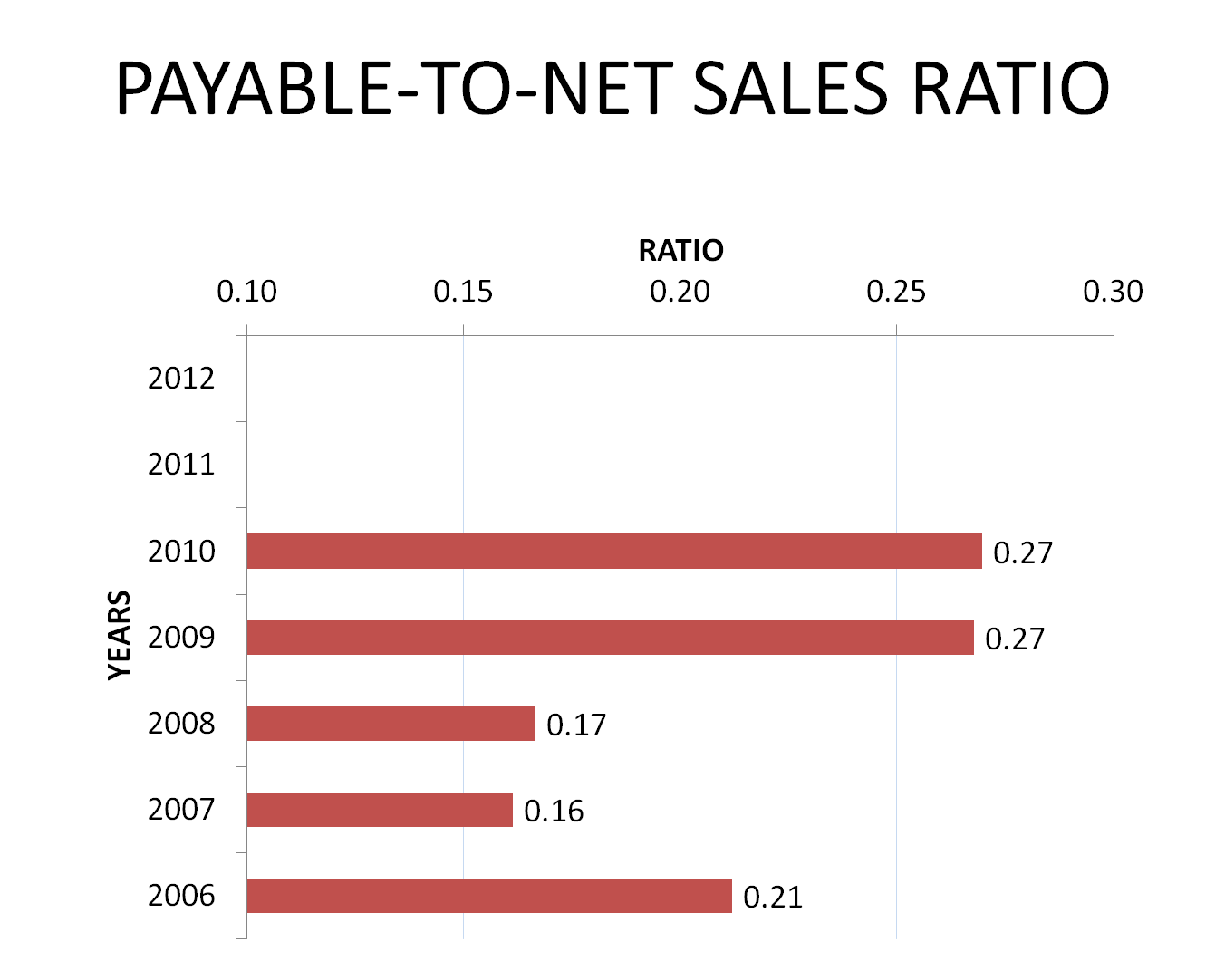

Efficiency (5) - Payable to Net Sales Ratio

|  |

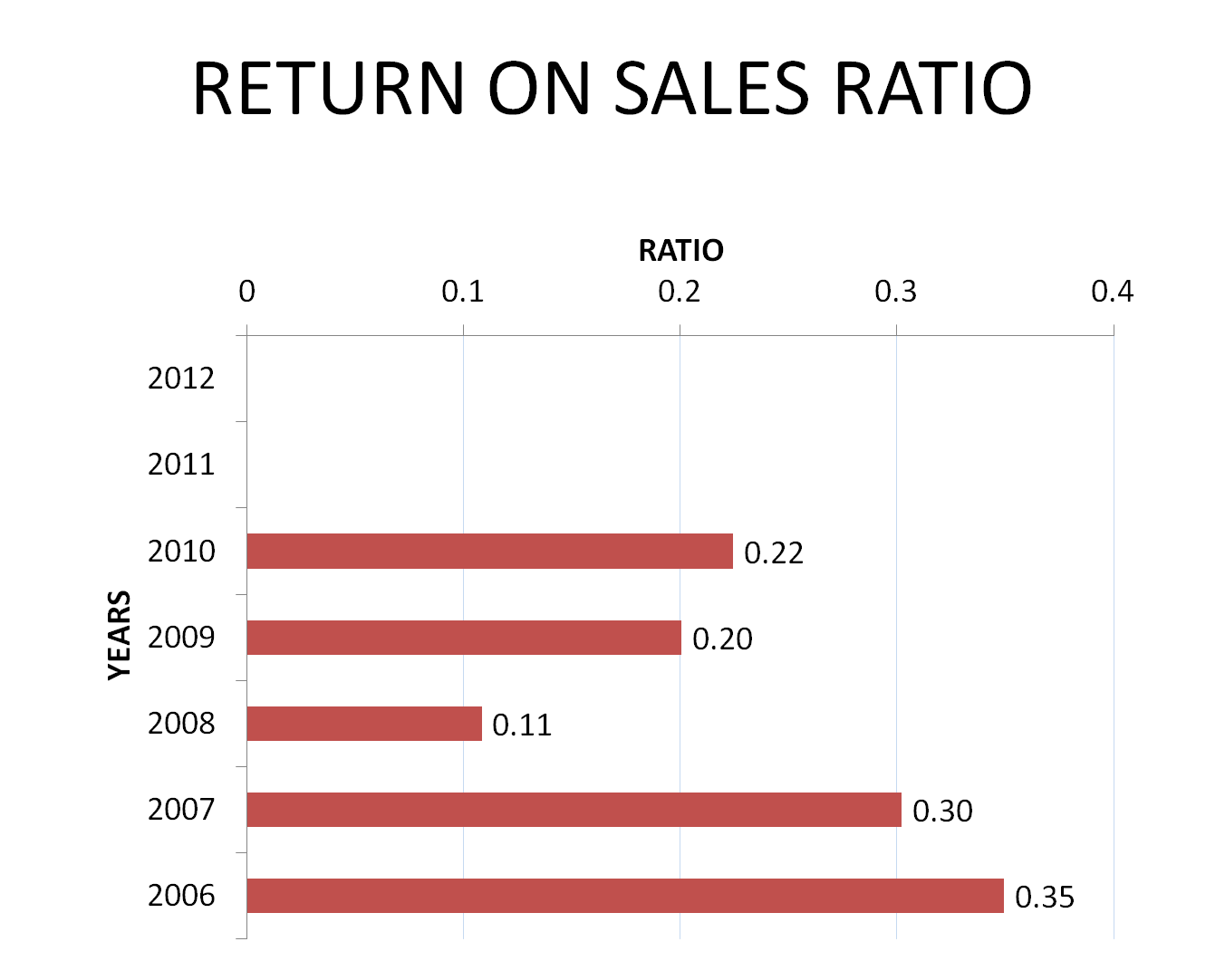

Profitability (1) - Return on Sales, or Profit Margin

|  |

Profitability (2) - Return on Assets

|  |

Profitability (3) - Return on Equity

|  |

One of the best things to do is to get in touch with financial analysis singapore based companies.

ReplyDelete